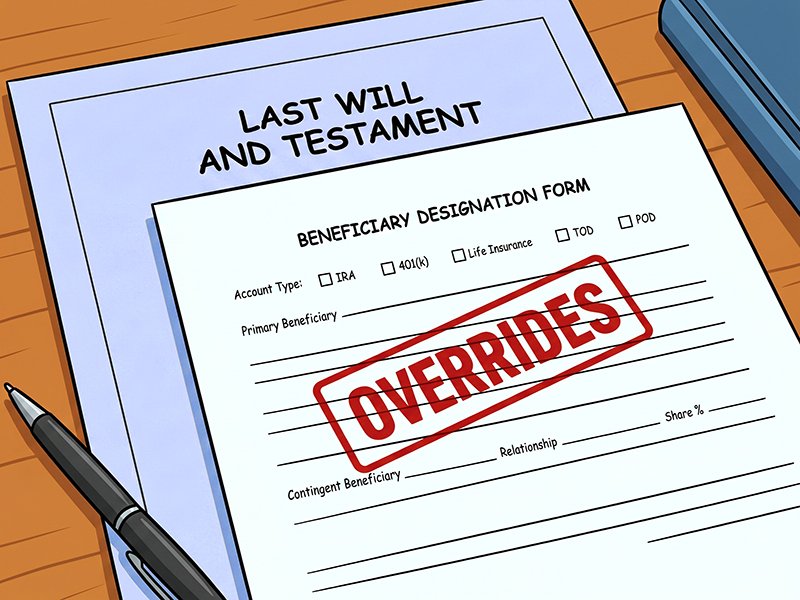

Most people think the most common estate-planning mistake is not having a will. This definitely happens more than it should. But the biggest mistake we see most often is this: someone has a brand-new will or trust that clearly says where assets are supposed to go, but their IRA, 401(k), life insurance, or brokerage account paperwork still says something different.

For assets that pass by beneficiary designation, the form on the account generally controls, not your brand-new will. If your will says everything should go to your spouse, be split evenly between your kids, or flow into a trust, but your IRA or 401(k) beneficiary form says something else, that old form attached to the account usually wins.

Bottom line: A brand-new estate plan does not automatically replace old beneficiary paperwork. And this is not limited to retirement accounts. On a brokerage account, TOD stands for transfer on death. It works a lot like a beneficiary designation. If a TOD has been added, that registration usually controls who inherits the account. If no TOD or POD has been added, do not assume the account has a beneficiary attached at all.

Checklist #1 – Accounts to review:

- IRAs, including old rollover IRAs

- 401(k)s and other employer retirement plans

- Life insurance policies

- Taxable brokerage accounts, especially those with TOD (transfer on death) instructions

- Bank accounts with POD (payable on death) instructions

- Joint accounts

- Old employer plans you have not looked at in years

Checklist #2 – Paperwork to compare:

- Your current will

- Your revocable trust, if you have one

- The primary beneficiary on each account

- The contingent beneficiary on each account

- The account titling or registration

- Any TOD or POD designations

- Any trust listed as beneficiary

This is the real checkup: does your estate plan say one thing while your account forms say another?

A quick note on joint and non-retirement accounts

Many joint accounts are set up with rights of survivorship, which means the surviving owner typically receives the account automatically at the first death. But the account agreement still matters, and not every joint account works the same way. In the right situation, a survivorship or transfer-at-death setup can be a simple option, especially when a lone parent has one intended child beneficiary and wants that account to pass directly. The right approach depends on how the account is set up and how it fits into the broader estate plan.

Checklist #3 – Common reasons the paperwork is stale

- You got married or remarried

- You got divorced

- A spouse or beneficiary passed away

- You had children or grandchildren

- One child was named years ago and the rest never got added

- You opened a new account and copied old instructions

- You named a parent when you were young and single and never revisited it

- You updated your will or trust, but nobody coordinated the accounts afterward

Common cleanup issues we see

- An ex-spouse is still listed

- One child is listed even though the intent is to treat kids equally

- No contingent beneficiary is listed

- A trust was supposed to receive the asset, but the account bypasses it

- A TOD or POD designation was added as a shortcut, but now it does not match the broader estate plan

- Different accounts tell different stories

Why retirement accounts deserve extra attention

This issue matters even more with IRAs and 401(k)s because beneficiary choices can affect tax treatment, timing, and flexibility. A surviving spouse often has more options than a non-spouse beneficiary, and many non-spouse designated beneficiaries are subject to the 10-year payout rule. In many 401(k) plans, the spouse is also the automatic beneficiary unless the spouse signs a waiver.

Where we help and where the attorney helps

In our role as financial advisors, we help our clients review beneficiaries, check titling, spot outdated TOD/POD instructions, and coordinate with your custodian and estate attorney. Your estate attorney handles the will, trust, trust language, legal interpretation, and state-specific estate law issues.

Bottom line

If your will or trust says assets should go one direction, but your beneficiary forms say something else, the beneficiary forms on those accounts will usually control.

So if it has been a few years since you reviewed your beneficiary forms, or if you have had a marriage, remarriage, divorce, death in the family, kids, grandkids, new accounts, or a new estate plan, this is worth a fresh look.

Reach out if you would like help reviewing your beneficiary designations, account titling, and estate documents to make sure they all line up. And if there is a beneficiary mistake or account type you think belongs on this checklist that I did not mention, let us know.