If you are self-employed and trying to choose between a SEP IRA and a Solo 401(k), here is my quick take:

For most owner-only businesses, or businesses where the only other employee is a spouse, we usually prefer the Solo 401(k).

Why? Because it often lets you save more at lower income levels, gives you catch-up contribution flexibility a SEP IRA does not have, and tends to work much better with Backdoor Roth planning. That does not mean the SEP IRA is bad. It is simpler. It is easier. And for some people, that is enough.

For what it is worth, I use a Solo 401(k) myself for three reasons: the ability to set more aside, the ability to move pre-tax IRA money into the plan so Backdoor Roth contributions are cleaner, and the fact that my wife can participate as an employee and potentially double the impact of the first two reasons. The Solo 401(k)s we use for clients are set up to accept eligible pre-tax IRA and SEP IRA rollovers, which is one of the reasons we like them so much for the right household. Check out our related post on how spouses can help make Solo 401(k)s even better.

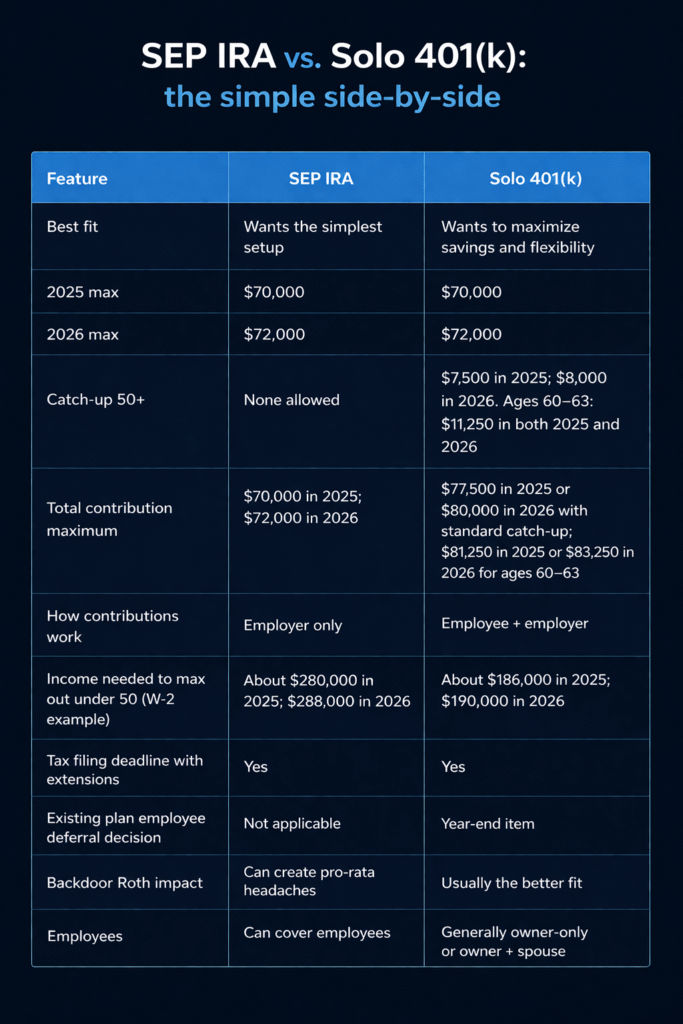

SEP IRA vs. Solo 401(k): The Simple Side-by-Side

Table note: the 2025 and 2026 limits, catch-up amounts, one-participant 401(k) rules, SEP timing rules, owner deferral timing rules, and Form 8606 treatment of SEP and traditional IRAs all come from IRS guidance.

Why We Usually Lean Solo 401(k)

The biggest reason is simple: it usually lets you save more on less income.

A SEP IRA is employer money only. A Solo 401(k) gives you an employee bucket and an employer bucket. That extra employee bucket is what usually changes the math. Using a simple S-corp example, an owner with $150,000 of W-2 wages could generally put away $37,500 into a SEP IRA. In a Solo 401(k), that same person could put away about $61,000 in 2025 or $62,000 in 2026, assuming no other salary deferrals elsewhere. Same income. Very different result.

It gets even more interesting for married couples when both spouses work in the business. Under that same simple W-2 framework, a couple would need about $560,000 of combined wages in 2025, or $576,000 in 2026, to max out two SEP IRAs. To max out two Solo 401(k)s, that same couple would need about $372,000 in 2025 or $380,000 in 2026. That is a huge difference, and it is one of the main reasons we like the spouse angle so much.

Why It Helps with Backdoor Roth Planning

SEP IRA balances live in the IRA bucket for pro-rata purposes. That means a SEP IRA can muddy up what otherwise would have been a clean Backdoor Roth contribution. A common move we make for the right client is to roll pre-tax IRA or SEP IRA dollars into the Solo 401(k), which can make future Backdoor Roth contributions much cleaner. That is one of the more practical reasons we often prefer the Solo 401(k) over the SEP IRA.

When the SEP IRA Still Makes Sense

The SEP IRA still wins the simplicity contest.

It is easier to open, easier to maintain, and can generally be set up and funded by the tax filing deadline, including extensions. So yes, that can mean after April 15 and as late as October if you extend. A Solo 401(k) can also allow funding by the tax filing deadline with extensions, but for an existing plan, the employee deferral decision is generally a year-end item.

So when does a SEP IRA still make sense? Usually when you want the easiest possible setup, income is high enough that you are still saving a lot, and you are not trying to optimize around Backdoor Roth contributions, catch-up contributions, or spouse participation.

One quick caution: if you have employees beyond a spouse, do not assume a Solo 401(k) is still the answer. One-participant 401(k)s are generally built for the business owner alone or the owner and spouse. Once other eligible employees enter the picture, you need to look at other options.

Bottom Line

For many owner-only businesses, the Solo 401(k) is simply the better tool.

It often allows larger contributions at lower income levels, gives you catch-up flexibility a SEP IRA does not have, works better for Backdoor Roth planning, and can become even more powerful when a spouse is involved in the business. That is why we usually prefer it.